UPDATE (May 2026): The Australian Government has confirmed a three-phase restructure of the EV FBT exemption. The full exemption continues until 31 March 2027. From 1 April 2027, a $75,000 price cap applies. From 1 April 2029, a 25% FBT discount replaces the full exemption for all eligible EVs.

Electric Car Discount Bill Approved

The Electric Car Discount Bill received royal assent on 12 December 2022. The following government charges are removed for electric vehicles, effective from 1 July 2022:

- Import tax on electric vehicles; and

- Fringe Benefits Tax - FBT on electric vehicles.

The FBT exemption will have the most profound and direct impact on the affordability of electric cars in Australia. Below is everything you need to know about the FBT exemption government incentive for electric cars.

FBT Exemption for Electric Vehicles - Key Features

✅ Eligible cars that are zero or low emissions vehicles are exempt from Fringe Benefits Tax (FBT) that are first held and used after 1 July 2022.

🚗 Zero or low emission vehicles

A vehicle is a zero or low emissions vehicle if it satisfies both of these conditions. It is a:

1. battery electric vehicle or hydrogen vehicle.

2. car designed to carry a load of less than 1 tonne and fewer than 9 passengers (including the driver).

🔌 Plug-in-hybrid vehicles where phased out from 31 March 2025. Learn more about the different electric vehicle types.

| Type | Definition |

| Battery electric vehicles | Battery-electric vehicles are any motor vehicle that only uses a high-density battery as its source of ‘juice’ and do not emit any pollutants from the tailpipe. |

📅 Vehicles are to be first held or used after 1 July 2022. If you ordered before this date and receive delivery after, you will be eligible.

2️⃣ A second-hand electric car may qualify for the exemption, provided it was first purchased new on or after 1 July 2022.

◀ Car value (includes delivery fees, accessories and options) must be below the Luxury Car Tax (LCT) threshold for fuel-efficient vehicles: <$91,387 for 2025/26.

📦 Applies to cars under salary packaging arrangements (including those procured under a novated lease).

⏳ The FBT exemption rules are now structured acros three phases:

- Phase 1 (now → 31 March 2027): Full exemption, no change

- Phase 2 (from 1 April 2027): Full exemption only for EVs under $75,000; EVs $75k–$91,387 receive a 25% FBT discount

- Phase 3 (from 1 April 2029): 25% FBT discount for all eligible EVs, no full exemption

What is Fringe Benefits Tax (FBT)?

Fringe benefits tax (FBT) is a tax that employers pay on benefits paid to an employee in addition to their salary or wages. Historically this included cars that are salary packaged via novated leases. FBT is calculated on the taxable value of the benefits you provide. This is separate to income tax.

With respect to salary-packaged cars, there is more often than not, a level of private use, which triggers an FBT obligation. According to the ATO, if a car is garaged at or near an employee’s home, it is taken to be available for the employee’s private use and is subject to FBT. FBT is effectively taxing the 'personal' benefit received from the use of the car outside of work purposes. You can read more about FBT works here.

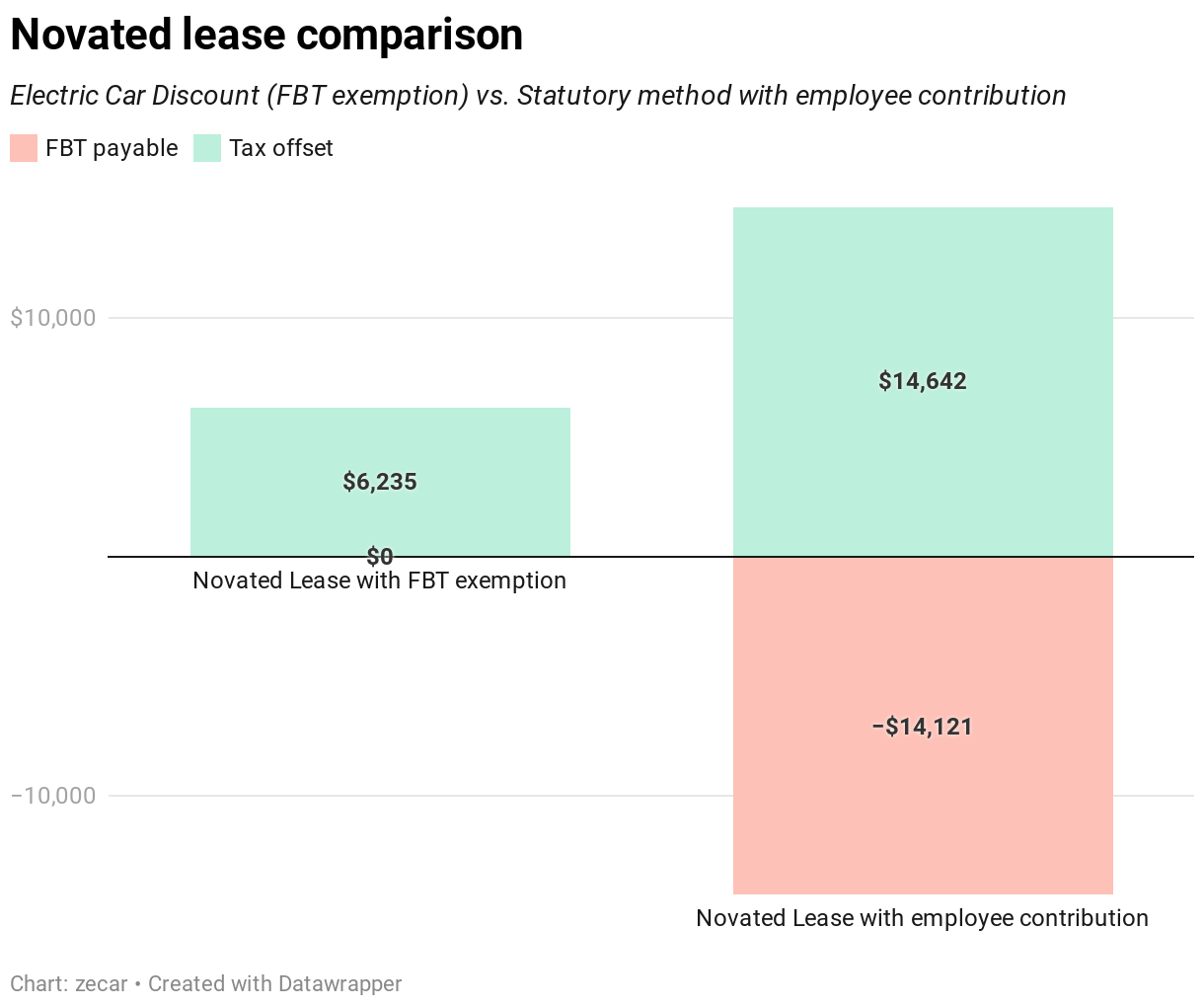

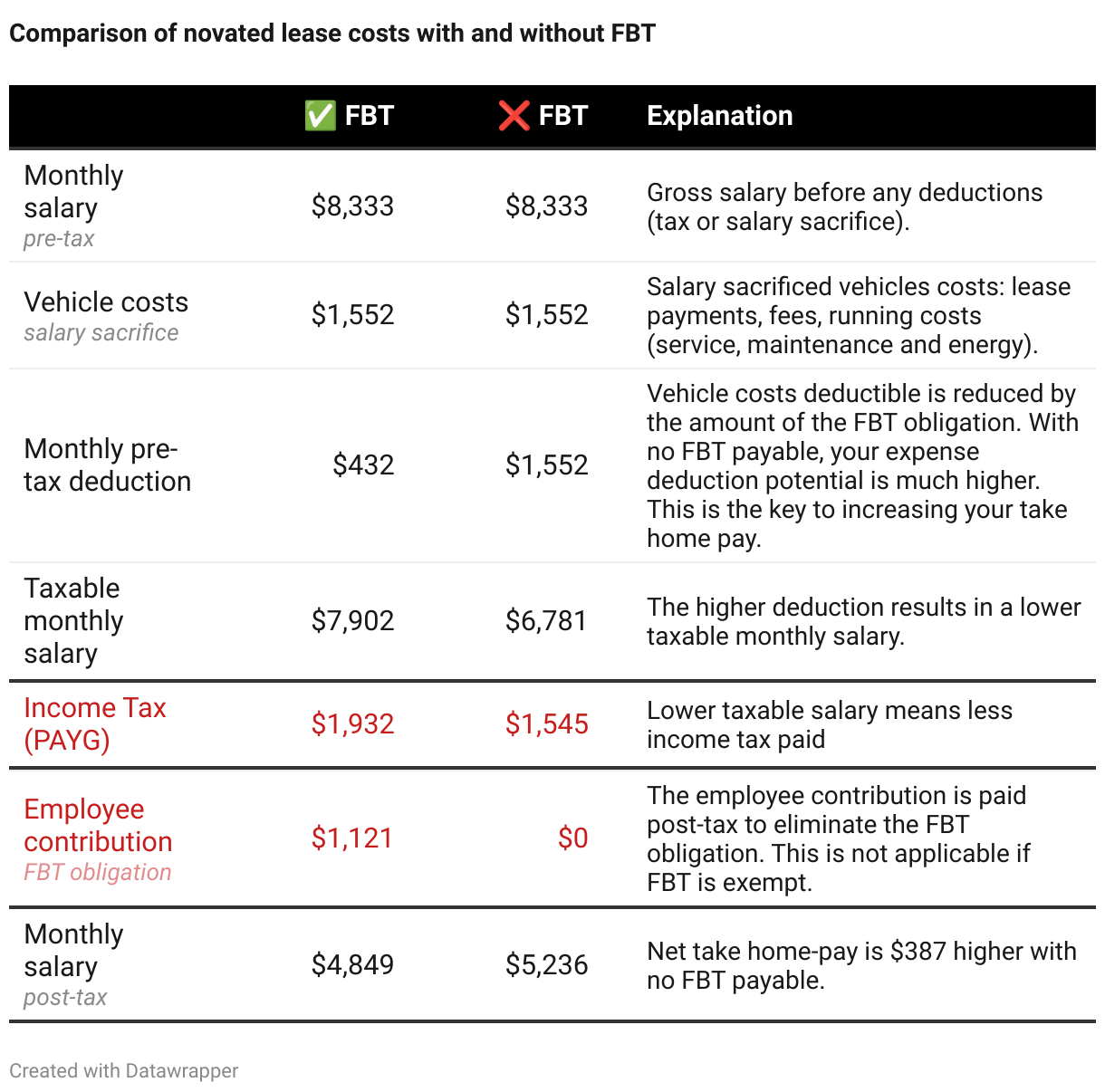

Following the introduction of the Electric Car Discount Bill, electric cars that are salary packaged will be exempt from FBT. This means you get the full tax benefit from the deductions without the FBT obligation attached. The chart below compares the tax treatment for a Tesla Model 3 RWD under an FBT exempt novated lease and one where FBT is payable. In this example, the FBT payable effectively wipes out almost all the benefits of the tax offset.

How Does the EV FBT Exemption Work?

The EV FBT exemption removes the need to pay fringe benefits tax on eligible electric vehicles on a novated lease. This has the effect of significantly increasing the potential tax savings.

Prior to the introduction of the EV FBT exemption, an FBT obligation would be triggered on a novated lease and an employee would typically use their post-tax salary to extinguish the obligation i.e. pay taxes. This has the effect of reducing the salary sacrificed amount and thus the potential income tax savings from a novated lease.

To illustrate the potential savings under for an FBT exempt electric car on a novated lease we’ll compare a novated lease with FBT payable and one without. Johnny works as a Sales Representative for a NSW-based company.

- Drives 15,000 km per annum

- Earns $100,000 gross income per annum

- Procure a Tesla Model 3 RWD ($63,900 MSRP) through a novated lease and a salary packaging arrangement through her employer

- Lease term is three years and the interest rate is 10%

Overall, Johnny stands to save $4,644 per annum and $13,932 over a three-year lease due to not needing to pay FBT.

How Much Will You Save Under an Electric Car Novated Lease?

The government estimates that “for individuals using a salary sacrifice arrangement to pay for the same model, their saving would be up to $4700 a year.” These figures are broadly in line with our calculations (below).

EV novated lease savings example

Below is sample report zecar provides its customers to demonstrate the benefits of an EV novated lease for their individual circumstances. In this case the customer is able to achieve over $25,000 of tax savings on a Tesla Model RWD over a three year lease compared to an outright purchase. This is attributable to the pre-tax salary deductions from the finance and running costs which reduces your taxable income and thus tax payable.

Read our guide on novated leases to learn more about how they work with electric cars.

Note: we are not privy to the assumptions used by the government’s modeling nor do we guarantee the accuracy of zecar’s estimates. These are for illustrative purposes only.

How Much Will Businesses Save?

According to advice from the government “a model valued at about $50,000 is provided by an employer through this arrangement, our fringe benefits tax exemption would save the employer up to $9000 a year”. These estimates are broadly in line with our calculations (outlined below).

For additional information on EV incentives for businesses:

Which Electric Vehicles are Exempt from FBT?

Below is a list of FBT exempt battery electric vehicles models for 2026.

LEARN MORE ➡ Electric Car Incentives in Australia: State-by-State Guide

Battery electric vehicles (BEVs) eligible for the FBT exemption

When Does the EV FBT Exemption End?

UPDATE: In March 2026, The government has now confirmed a three-phase restructure of the EV FBT exemption. The full exemption will not be scrapped outright, but will be progressively scaled back.

Phase 1 (Now → 31 March 2027): No change

The existing rules remain in place. The LCT threshold for fuel-efficient vehicles ($91,387 in 2025/26) continues to apply as the eligibility cap.

Phase 2 (From 1 April 2027): $75,000 price threshold introduced

EVs priced below $75,000 retain the full FBT exemption. EVs priced between $75,000 and the LCT threshold ($91,387) receive a 25% FBT discount only — not full exemption.

Phase 3 (From 1 April 2029): 25% discount for all eligible EVs

The full exemption ends for all vehicles. All eligible EVs under the LCT threshold receive a 25% FBT discount. Even the most affordable EVs (e.g. BYD Atto 1) will no longer qualify for the full exemption.

What about existing leases? Existing novated leases are grandfathered — if your lease was entered into before the relevant phase start date, the new rules do not apply to it.

For the full breakdown including worked dollar examples, see: EV Tax Break Extended: What the Confirmed Changes Mean for Buyers

Frequently Asked Questions

About the author

Danny is a consultant and entrepreneur working at the cutting edge of the electric vehicle and energy transition. He is passionate about educating and helping consumers make better decisions through data.